With the Federal Budget just around the corner, all eyes will be on the government to find the right balance of the ongoing cost-of-living pressures amid the uncertainty of the current economic climate.

In the meantime, here is our latest newsletter.

If you are considering investing but haven’t started your journey, we have outlined 7 simple steps that could help you achieve your investment goals.

From 1 July 2026, Payday Super will come into effect. If you have an SMSF, take the time to find out how these changes may impact you. Discover more in this article.

With the recent share market turbulence, we explain exactly what it is, how it’s measured and what you need to consider during periods of market volatility.

If retirement is on the horizon, you may be considering what your retirement income options are. In this article, we’ve outlined the different income sources that could help you feel more secure during your twilight years.

And finally, we explore the world of ‘Blue Zones’. As the myth fades, a clearer and more practical picture of healthy aging comes into focus.

7 simple steps to get on the investment ladder

7 simple steps to get on the investment ladder

Entering the world of investing can be a life-changer for people of all ages. Here are seven simple steps for beginners to start their wealth journey.

1. Do a financial stocktake

Before taking the leap into investing, evaluate your financial position. Assess your income, savings, living expenses and, perhaps most importantly, your personal debts (you may focus first on clearing high-interest credit card debt). An honest assessment will give you clarity about the funds you have available to invest.

2. Set your goals

Are you saving for a home deposit? Travel? Retirement? Long-term wealth? Having real targets enhances your prospects of success. During this early phase, seeking the guidance of an experienced financial adviser to help lay your investment foundations can pay dividends. This is where we can assist.

3. Determine your risk profile

Investing carries an element of risk. How much market volatility can you handle? Could you sleep at night if your share portfolio dropped 20%? Risk profiles and goals can differ markedly from person to person, depending on income levels and lifestyle and retirement goals. Some investors want a simple, low-risk managed fund. Others may want to take more risks on potentially high-return tech stocks, for example.

4. Start small and contribute consistently

You do not need a large lump sum to start investing. One common approach is making manageable, regular contributions to benefit from compounding growth, which accumulates over time and can help build long-term wealth.

5. Diversify your assets

Diversification is a tried-and-tested investment strategy that can reduce your portfolio’s overall risk and volatility. This entails investing in different asset classes, sectors and geographies to spread your risk and reduce the overall portfolio impact if one sector fails or performs badly.

6. Understand your asset class options

The key portfolio options are as follows:

-

Shares – by buying shares, investors become part owners in companies and can benefit if the company increases in value or pays dividends.

-

Bonds – when governments or corporations want to borrow money, they can issue bonds, which are securities that usually pay investors a fixed interest rate.

-

Cash – a low-risk, short-term financial instrument that typically provides stable and regular income through interest payments.

-

Managed funds – an investment where your money is pooled together with other investors and managed by a professional.

-

ETFs – an ETF is a pooled investment vehicle that you can buy or sell on an exchange, like the Australian Securities Exchange. In Australia, most ETFs are low-cost, index-tracking investments.

7. Keep learning and reviewing

Educate yourself about market basics, fees and investment options. Once you have a portfolio set up, regularly review it to ensure it still matches your risk appetite and goals.

To begin your investment journey, reach out to us today.

Source: Vanguard April 2026

This article has been reprinted with the permission of Vanguard Investments Australia Ltd. Copyright Smart Investing™

GENERAL ADVICE WARNING

Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) (VIA) is the product issuer and operator of Vanguard Personal Investor. Vanguard Super Pty Ltd (ABN 73 643 614 386 / AFS Licence 526270) (the Trustee) is the trustee and product issuer of Vanguard Super (ABN 27 923 449 966).

The Trustee has contracted with VIA to provide some services for Vanguard Super. Any general advice is provided by VIA. The Trustee and VIA are both wholly owned subsidiaries of The Vanguard Group, Inc (collectively, “Vanguard”).

We have not taken your or your clients’ objectives, financial situation or needs into account when preparing our website content so it may not be applicable to the particular situation you are considering. You should consider your objectives, financial situation or needs, and the disclosure documents for the product before making any investment decision. Before you make any financial decision regarding the product, you should seek professional advice from a suitably qualified adviser. A copy of the Target Market Determinations (TMD) for Vanguard’s financial products can be obtained on our website free of charge, which includes a description of who the financial product is appropriate for. You should refer to the TMD of the product before making any investment decisions. You can access our Investor Directed Portfolio Service (IDPS) Guide, Product Disclosure Statements (PDS), Prospectus and TMD at vanguard.com.au and Vanguard Super SaveSmart and TMD at vanguard.com.au/super or by calling 1300 655 101. Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance. This website was prepared in good faith and we accept no liability for any errors or omissions.

Important Legal Notice – Offer not to persons outside Australia

The PDS, IDPS Guide or Prospectus does not constitute an offer or invitation in any jurisdiction other than in Australia. Applications from outside Australia will not be accepted. For the avoidance of doubt, these products are not intended to be sold to US Persons as defined under Regulation S of the US federal securities laws.

© 2026 Vanguard Investments Australia Ltd. All rights reserved.

Payday Super Regulations: further details for SMSFs

Payday Super Regulations: further details for SMSFs

If you have an SMSF, find out how the new Payday Super Regulations will impact SMSFs when Payday Super starts from 1 July 2026.

With the Payday Super Regulations starting from 1 July 2026, take the time to see how the changes will impact your SMSF.

Contribution allocations: a closer look

SMSFs will still have up to 28 calendar days after the end of the month in which a contribution is received to allocate or return super contributions. This has not changed as a result of the Regulations.

Super funds will have 3 business days (reduced from 20 business days) to allocate or return super contributions.

Other key details in the Regulations

-

Confirmation of which types of payments are excluded from qualifying earnings (payments that don’t attract superannuation guarantee).

-

Provides details on how the administrative uplift amount, included within the super guarantee charge calculation, may be reduced.

These Regulations supports planned SuperStream improvements, including:

-

clearer error messaging

-

the new Member Verification Request (MVR) so employers can confirm fund details before paying

-

New Payment Platform (NPP) enabled payments.

What SMSFs should do

All funds and SMSFs must be ready for Payday Super by 1 July 2026. Make sure your electronic service address (ESA) provider continues to support the updated SuperStream standards so your SMSF can keep receiving contributions on time.

For more information, speak to us or visit ato.gov.au/paydaysuper.

Source: ATO.gov

Reproduced with the permission of the Australian Tax Office. This article was originally published on https://www.ato.gov.au/newsroom/smallbusiness/

Important: This provides general information and hasn’t taken your circumstances into account. It’s important to consider your particular circumstances before deciding what’s right for you. Although the information is from sources considered reliable, we do not guarantee that it is accurate or complete. You should not rely upon it and should seek qualified advice before making any investment decision. Except where liability under any statute cannot be excluded, we do not accept any liability (whether under contract, tort or otherwise) for any resulting loss or damage of the reader or any other person. Any information provided by the author detailed above is separate and external to our business and our Licensee. Neither our business nor our Licensee takes any responsibility for any action or any service provided by the author. Any links have been provided with permission for information purposes only and will take you to external websites, which are not connected to our company in any way. Note: Our company does not endorse and is not responsible for the accuracy of the contents/information contained within the linked site(s) accessible from this page.

What is share market volatility

What is share market volatility

Volatility is how the return on an asset fluctuates over time. Using the share market as an example, volatility is often measured by changes in the price of a share. When the market is volatile, as it has been recently due to the geopolitical tensions in the Middle East, prices can rise or fall a lot in a short time.

These movements mean the value of your investments can change quickly. They might rise in value one day and fall the next.

Volatility can make us feel nervous, but short-term ups and downs happen often in share markets. Over long periods, markets have moved through many cycles of rises and falls.

Check out this chart from the Australian Securities Exchange (ASX) showing an example of Australian share price movements between 1995 and 2025.

What causes share market volatility?

As the ASX chart linked in the smart tip box shows, a lot of factors can move share prices quickly.

Share markets respond to new information such as economic data, company results and global events. Investors react to this information by buying and selling shares, which moves prices.

Economic data often affects the market. Changes in interest rates, inflation or economic growth can shape how investors view the future performance of companies.

Global events also influence markets. Political decisions, trade changes or international conflicts can create uncertainty for investors.

Investor behaviour can also drive volatility. When many investors feel nervous, they may sell shares at the same time, which can push prices down. When investors feel more confident, they may buy more shares and push prices up.

Because new information appears all the time, the price of listed shares can change frequently.

What to consider when markets are volatile

Large changes in share markets market movements can make us feel nervous, but quick reactions to market swings can sometimes lead to poorer long term decisions. So:

-

Focus on your goals. Markets move in the short term, but many people invest for the long term. Make sure you match your investments to your goals, timeframe and risk level, and review your investment plan regularly.

-

Avoid emotional decisions. Selling investments during a fall can ‘lock in’ losses. And making emotional decisions might also make you a target for scams.

-

Stay diversified. Spread your money across different investments such as shares, property, bonds and cash to help reduce risk.

-

Seek advice if you need it. We can help you understand your options.

A clear plan can help you stay focused when markets move up and down.

Be on red alert for phone calls, click bait advertising and promises of unrealistic returns to encourage you to put your super into risky investments. High-pressure sales tactics may be putting your super savings at risk. Stop, think carefully, and check the claims first, or call us if you are unsure.

Reproduced with the permission of ASIC’s MoneySmart Team. This article was originally published at https://moneysmart.gov.au/how-to-invest/what-is-share-market-volatility

Important note: This provides general information and hasn’t taken your circumstances into account. It’s important to consider your particular circumstances before deciding what’s right for you. Although the information is from sources considered reliable, we do not guarantee that it is accurate or complete. You should not rely upon it and should seek qualified advice before making any investment decision. Except where liability under any statute cannot be excluded, we do not accept any liability (whether under contract, tort or otherwise) for any resulting loss or damage of the reader or any other person. Past performance is not a reliable guide to future returns.

Important

Any information provided by the author detailed above is separate and external to our business and our Licensee. Neither our business nor our Licensee takes any responsibility for any action or any service provided by the author. Any links have been provided with permission for information purposes only and will take you to external websites, which are not connected to our company in any way. Note: Our company does not endorse and is not responsible for the accuracy of the contents/information contained within the linked site(s) accessible from this page.

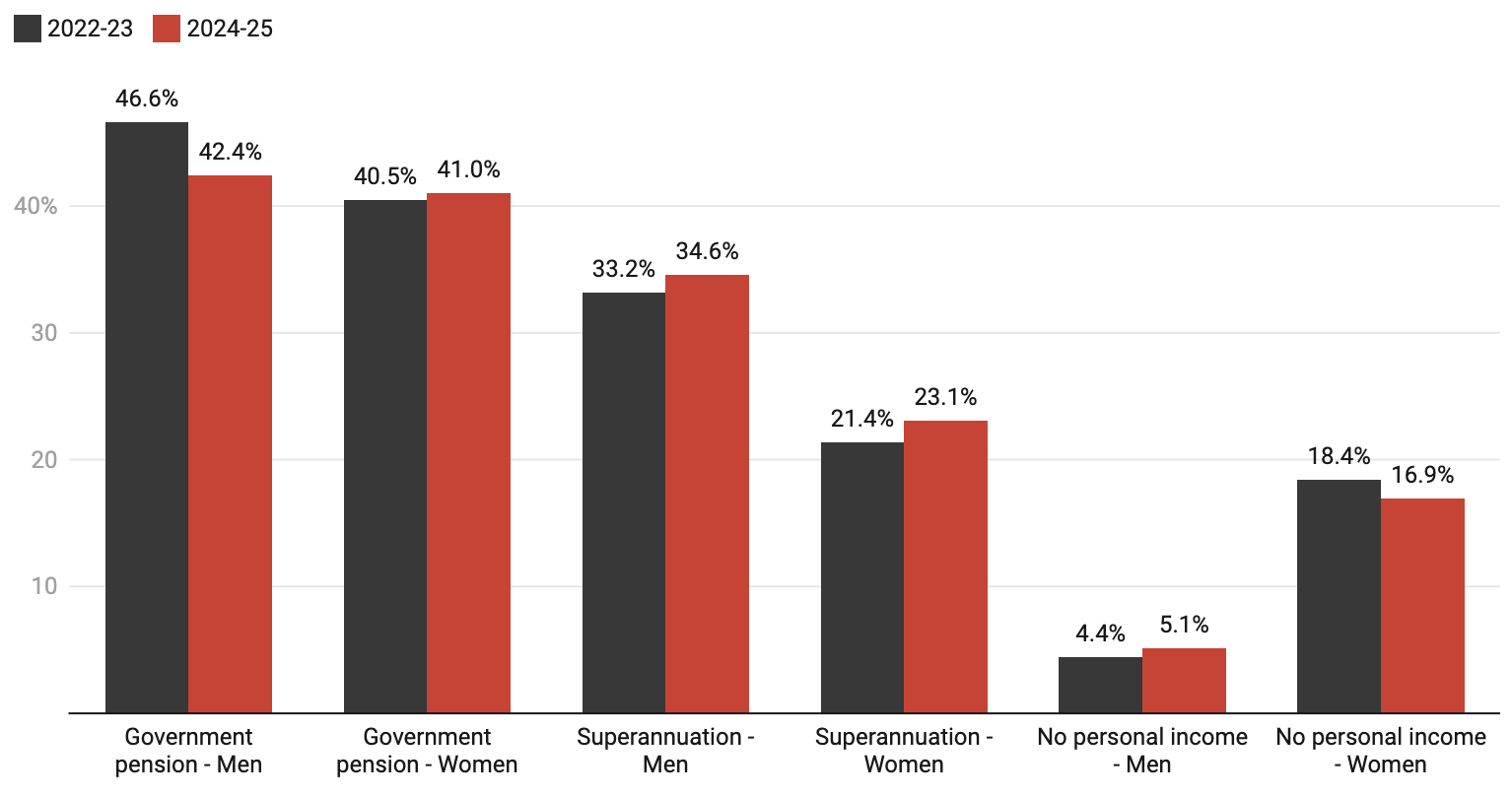

I’m close to retirement age. What are my options for drawing on my super savings?

I’m close to retirement age. What are my options for drawing on my super savings?

Retiring well means making a series of decisions to ensure a financially secure post-work life. One practical step is to work out the income you need each week to survive and thrive when you stop working.

If you are one of the many Australians still working and growing your super, knowing more about tailored retirement income products might help to plan.

There are two main ways to use super savings in retirement:

-

through products that provide an income stream, and/or

-

through lump sums.

Account-based pensions

The most common product for a retirement income stream in super is an account-based pension. These can be set up outside super, but there are advantages inside super. Around 80% of retired super fund members have one or more account-based pensions in super.

These products offer flexibility, control and continued exposure to investment markets. They allow retirees to convert part, or all, of their super balance into an income stream while keeping an allocated sum invested.

More than one can be set up, at different times, and with different investment choices, so your investment balance keeps growing while providing income in the short-term. Retirees can choose how much they withdraw, as long as they meet the government’s minimum withdrawal requirements.

Arguably, the greatest advantage of an account-based pension within super is its tax effectiveness compared to investments outside super. Once a super member is fully retired, both the investment earnings and income drawn from an account-based pension in super is tax-free.

One of the disadvantages of account-based pensions in super is that the age-based minimum drawdown rates might not suit your investment timing or income preferences. Investment returns are not guaranteed, and you don’t know how many years of income will be needed.

If you die before the funds are fully drawn, however, your beneficiary can receive the remaining money.

Another option for regular income: annuities

Retirees can also use their super to buy another type of income product called an annuity. There are a few main types of annuities and you can choose if you want the income payments:

-

guaranteed over a fixed period of time

-

investment-linked over a fixed period or for life, or

-

guaranteed for the rest of your life, typically adjusted for inflation.

The cost of the annuity will vary depending on these factors. Annuities provide more certainty both in the payments and timeframe for income, regardless of investment market performance.

In Australia, fewer than 5% of super member accounts are annuities. But that may be changing, as more retirees realise the advantages of including an annuity in their super income planning.

Annuities can be bought using super or non-super money, but using super has the advantage of tax-free earnings and income.

In addition, for Age Pension eligibility, Centrelink only takes into consideration 60% of the value of a lifetime annuity compared to 100% of an account-based pension. This favourable treatment means your super savings can last longer, because your retirement income will be supplemented with more Age Pension.

On the downside, annuities have less flexibility. Once you have committed a lump sum of super to purchase the annuity, you cannot convert that back into a lump sum.

The income from annuity returns may also not be as high as in an account-based pension, because there is a trade-off between investment returns and guaranteed income.

Choosing the right mix for your circumstances

Retirees may benefit from a retirement income strategy that includes a combination of account-based pensions and annuities, depending on their personal needs and circumstances.

Once aged 67, retirees will also be eligible for the Age Pension, within asset or income limits. More than 60% of retirees receive at least some Age Pension, around 40% as their main income.

Main source of income at retirement

The government Age Pension is the most common source of income for retirees, while 30% of retired women relied on their partner’s income to meet their living costs at retirement.

There is a maximum amount that can be transferred to pension phase within super, regardless of whether you choose an account-based pension or annuity, or a combination. That cap currently sits at A$2 million.

What about lump sums?

Once a super fund member reaches preservation age, usually age 60, and ceases at least one job, they may be able to access some or all their super as a lump sum. Alternatively, a member can access some or all their super as a lump sum when they turn 65, regardless of their employment.

With more people heading into retirement with mortgages, lump sums can be used to pay down debt, or for home repairs, holidays or even gifting.

How the lump sum is used may affect your age pension. In 2025, the average lump sum taken out by newly retired members was around $58,000.

While income stream products have a range of advantages within super, taking at least some super as a lump sum is common, even later in retirement. More than $71 billion was paid out in lump sums from superannuation in 2025 across 2.26 million member accounts.

Advice can help

Getting advice on coordinating super income streams and age pension entitlements can make a big difference to maximising your income while managing risk. Financial advice is in high demand, either within or outside your super fund.

Super funds can provide a range of valuable information, calculators and support. Other online tools are also available that can help with retirement income planning, including taking Age Pension eligibility into account.

For more information about your income in retirement, reach out to us.

Source: The Conversation

Blue Zones: lessons for living longer

Blue Zones: lessons for living longer

For years, the idea of “Blue Zones” captured the world’s imagination. Certain regions such as Okinawa, Sardinia, Ikaria and Nicoya were said to be places where people routinely lived past 100 years old in good health. The promise was simple and compelling: follow their lifestyle, and a long, vibrant life might follow.

In recent years, however, that story has become more complicated.

A necessary reality check

New research has raised questions about the original Blue Zones claims. Demographic researcher Dr. Saul Newman, who won an Ig Nobel Prize, suggests that many reported longevity hotspots overlap with regions of poverty, low literacy, weak birth record systems and clerical errors.i In some cases, people may not have been as old as records claimed, or ages may have been exaggerated for social or financial reasons.

The idea that these areas uniquely produce extraordinary numbers of centenarians is far less certain than once believed.

And yet, even if Blue Zones are not proven longevity hotspots, they may still point toward habits that support longer and healthier lives.

Longevity as a side effect of living well

One insight that remains remarkably consistent across cultures is that people who live long, healthy lives rarely make longevity their primary goal.

A strong sense of purpose has been repeatedly linked to lower mortality, reduced risk of cardiovascular disease, and better mental health. Whether described as ikigai, plan de vida, or simply feeling useful and needed, purpose appears to be protective regardless of geography and it does not require a grand mission. It can come from caring for others, creating something meaningful, contributing to a community, or continuing to learn and grow.

Movement is part of daily life

Blue Zones popularised the idea of natural movement, and while the framing may have been romanticised, the underlying principle is supported by science.

Large population studies consistently show that frequent, low intensity movement throughout the day is associated with lower risk of heart disease, diabetes, and early death. Long periods of sitting, even among people who exercise regularly, are linked to worse health outcomes.

The lesson is not that formal exercise is unnecessary. It is that health is supported most reliably by movement that is regular, functional, and woven into everyday life.

Simple approach to diet

The diets associated with Blue Zones vary widely, but they share some broad characteristics that align well with modern nutritional science. These patterns emphasise whole foods, especially vegetables and legumes, limited intake of ultra processed products, and moderate calorie consumption.

Just as important as what people eat is how they eat. Meals are often social and treated as a meaningful part of the day rather than a task to get through. This approach supports metabolic health, digestion, and long-term weight stability without relying on restriction or obsession.

Social connection as a foundation for health

One of the strongest and most consistent findings in health research is the impact of social connection.

Loneliness and social isolation are associated with higher risk of early death, depression, cognitive decline, and cardiovascular disease. Strong relationships, on the other hand, support immune function, emotional regulation, and resilience during periods of stress.

Humans thrive when they are connected to others and people feel they matter to others.

Stress is inevitable, recovery is essential

The idea that people in so called Blue Zones lived stress free lives is almost certainly inaccurate. Many of these regions faced economic hardship, uncertainty, and physical demands.

What appears to matter is not the absence of stress, but the presence of regular recovery. Rest, social time, spiritual practices, time outdoors, and predictable daily rhythms all help regulate the nervous system and reduce the long-term damage caused by chronic stress.

Health is shaped not just by what challenges we face, but by being able to return to a state of balance.

Beyond the myth

We can let go of the myth that there are magical places where people effortlessly live to extreme old age because of secret habits or perfect lifestyles. What we can keep is a grounded, evidence-based understanding of what supports health across cultures.

Living well for longer is not about chasing an extraordinary lifespan. It is about staying engaged with life, maintaining connection, and preserving physical and mental capacity for as long as possible.

That goal does not depend on where you live.

It depends on how you live.